What credit score do landlords look for? Across the rental industry, a minimum in the mid-600s is the most common benchmark, with higher bars for higher-rent homes and conditional approvals below it.

That number is common practice, not law, and it is not a Sagareus standard. In Washington, the legal requirement is different. Your written screening criteria must state your minimum and your denial conditions before you screen, and you must apply them identically to every applicant.

What Credit Score Do Landlords Look For? The Honest Answer

There is no statutory minimum credit score for renting a home in Washington, and no "correct" number. What exists is industry habit: many owners and property managers treat the mid-600s as the line for a clean approval, approve conditionally somewhere below that, and decline well below it.

Treat those figures as a starting point for setting your own standard, not as a rule. The right threshold for your property depends on the rent level, your tolerance for conditional approvals, and what the rest of your criteria already cover, such as income ratio and rental history.

Two things matter more than the number you pick. First, that you write it down before you accept applications. Second, that you never bend it for one applicant and enforce it against another. Consistency is what keeps a credit standard lawful; the specific threshold is a business decision.

What a Credit Score Actually Measures, and What It Does Not

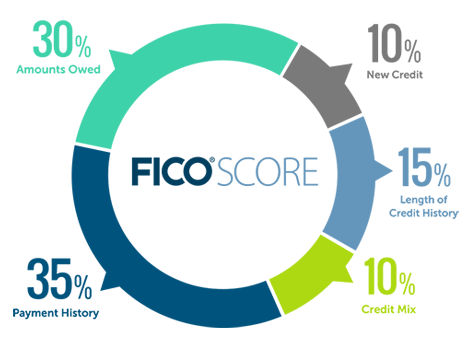

A credit score is a payment-reliability signal, not a character report. FICO, the most widely used scoring model, builds its 300 to 850 score from five factors:

- Payment history (35%). Whether the person pays obligations on time. This is the slice that overlaps most with rent.

- Amounts owed (30%). How much of their available credit they are using.

- Length of credit history (15%). How long their accounts have existed. This quietly penalizes young applicants and recent arrivals who may be excellent tenants.

- Credit mix (10%) and new credit (10%). Variety of account types and how recently they applied for credit.

Notice what is missing: nothing in that formula knows whether the applicant has ever paid rent, taken care of a home, or given proper notice. A score also cannot distinguish life circumstances from habits. A medical emergency, a divorce, or a student loan balance can drag a score down without saying anything about how that person treats a landlord.

Read the score as a flag, not a verdict. The score tells you where to look. The report tells you what actually happened.

Read the Full Report, Not Just the Number

Two applicants with the same 640 can be entirely different risks. The patterns underneath the number are where tenancy risk actually lives:

Two applicants with the same 640 can be entirely different risks. The patterns underneath the number are where tenancy risk actually lives:

- Collections from a prior landlord or property manager. This is the highest-signal item on any credit report for our purposes. It usually means someone left owing rent or damages and never resolved it. Weight it accordingly in your written criteria.

- Utility collections. Unpaid power, water, or internet bills track closely with how someone handles housing obligations. A pattern here deserves more attention than a single old retail account.

- Recent versus old delinquencies. A string of late payments in the last six months tells you about the applicant today. A rough patch four years ago followed by clean history tells you about recovery. Your criteria can lawfully distinguish the two; many well-written criteria do.

- Medical debt and student loans. These read differently than consumer defaults. Medical collections typically reflect an event, not a habit, and student loan balances are often large by design. Many owners weight them lightly compared to a landlord collection of one tenth the size.

If you want the full picture of what a screening file should include beyond credit, our pillar guide to tenant screening in Washington State walks through every component, from income verification to rental references.

How Credit Fits Into Lawful Written Criteria

In Washington, you cannot screen first and decide your standards later. Under RCW 59.18.257, before you obtain any screening information you must give applicants written notice (or a posting) covering:

- What types of information you will access in screening;

- What criteria may result in denial, which is where your credit minimum and your specific denial conditions belong;

- If you use a consumer report, the name and address of the consumer reporting agency and the applicant's rights to a free copy after a denial or other adverse action and to dispute inaccurate information;

- Whether you accept comprehensive reusable tenant screening reports. If you advertise rentals on a website, that statement must also appear on the property's home page, and if you accept them, you may pull your own report but may not charge the applicant for it.

You may only charge a screening fee at all if you gave that notice first. Your criteria, for example "minimum 650, no unresolved landlord collections, no more than X late payments in the past 12 months," should exist on paper before the first application arrives, and the same test should run on every applicant in the same way.

One statewide trap to avoid: source of income is a protected class in Washington under RCW 59.18.255. If an applicant has a voucher or subsidy, subtract it from the rent before applying your income ratio to their share.

Getting this wrong is expensive, with penalties up to 4.5 times the monthly rent plus costs and fees. Seattle layers on additional screening requirements, including its first-in-time rule, so verify current rules on seattle.gov before screening a Seattle property.

For the broader framework of building criteria that hold up, see our guide to tenant screening best practices.

When Credit Is Thin or Damaged: Lawful Conditional Paths

A below-threshold score does not have to mean a denial, and in a tight market it often should not. Washington's adverse action framework explicitly contemplates approval with conditions, including a qualified guarantor, last month's rent, an increased deposit, or an increased monthly rent.

The two most useful levers for credit-driven conditions:

- A qualified guarantor or co-signer. The cleanest path for thin files: students, new arrivals, and applicants who simply have not used much credit. Define in your written criteria what "qualified" means, such as the income ratio and credit standard the guarantor must meet.

- An increased deposit. Useful where the file shows damage rather than absence. But know your city: Seattle, Kirkland, Kenmore, Shoreline, and Auburn cap total move-in costs at one month's rent, which takes the larger-deposit lever off the table there. In cap cities, the guarantor path does the work instead.

The rule that makes conditional approvals safe is the same one that governs everything else: the conditions live in your written criteria, mapped to specific findings, and trigger the same way for everyone. "Score between 600 and 649 requires a qualified guarantor" is a policy. Deciding on the phone that this particular applicant seems nice enough to skip it is an ad-hoc exception, and ad-hoc exceptions are how Fair Housing complaints start.

The Adverse Action Notice: Your Duty When Credit Drives the Decision

Whenever credit causes you to deny an application or approve it with conditions, Washington law requires a written adverse action notice in the statutory format set out in RCW 59.18.257. It must state the reasons, and the statutory form includes checkboxes for both outright rejection and approval with conditions such as an increased deposit, a qualified guarantor, last month's rent, or increased monthly rent.

When a consumer report contributed to the decision, the notice must include the name, address, and phone number of the consumer reporting agency that furnished it. Skipping the notice can cost up to $100 plus court costs and attorney fees per violation, and it is the single most commonly missed step among self-managing owners.

Federal law layers on top. Under the Fair Credit Reporting Act, per the Consumer Financial Protection Bureau, an applicant denied (or conditioned) based on a screening report must be told, given the reporting company's contact information, informed of the right to a free copy of the report if requested within 60 days, and informed of the right to dispute inaccurate information.

Conditions count: requiring a co-signer or a larger deposit because of the report is adverse action under federal law too, not just a denial.

A denied applicant who disputes and fixes a report error is exercising a legal right, not causing trouble. Build the notice into your process so it goes out every time, automatically. If a denial later escalates into a dispute or a holdover situation, our guide to the eviction process in Washington State covers what proper documentation buys you.

Credit Myths Owners Still Believe

"Running a credit check will hurt my applicant's score." Usually not. The CFPB distinguishes hard inquiries, which follow applications for credit and do affect scores, from soft inquiries, which include screening reviews and do not affect scores. Many tenant screening products are structured as soft pulls; confirm with your screening provider which type they use before you reassure an applicant.

"No score means high risk." A thin file means little borrowing history, not bad history. Length of credit history is 15% of a FICO score, so young applicants and recent arrivals start at a structural disadvantage. Verified income and strong rental references can tell you more than an empty credit file ever could; a guarantor condition covers the gap.

"There is one official score." Different scoring models and versions produce different numbers for the same person. The score on your screening report may not match the one on the applicant's banking app, and neither is "wrong." This is another reason your criteria should name the patterns that matter, not just a single number.

"A minimum score is required, so my hands are tied." No law sets a minimum credit score. The minimum is yours to choose; the law governs how you disclose it, apply it, and give notice when it drives a decision.

Frequently Asked Questions

What credit score should I require for my rental?

There is no legally required number. A mid-600s minimum is the most common industry benchmark, with conditional approval bands below it. Pick a threshold that fits your rent level and risk tolerance, write it into your screening criteria along with the specific conditions that trigger denial or conditional approval, and apply it identically to every applicant.

Can I deny an applicant for medical debt?

Credit-based criteria may lawfully result in denials when they are written, disclosed before screening, and applied uniformly. That said, medical debt is a weak predictor of rent payment compared to landlord or utility collections, and scoring models have been reducing its weight. Many owners deliberately exclude or discount medical collections in their written criteria; whatever you choose, the rule must be the same for everyone.

Do I have to tell an applicant why they were denied?

Yes. Washington's RCW 59.18.257 requires a written adverse action notice stating the reasons, in a statutory format, whenever you deny or approve with conditions. If a consumer report contributed, you must include the reporting agency's name, address, and phone number, and federal law gives the applicant the right to a free copy of the report on request within 60 days and to dispute errors.

Does checking an applicant's credit lower their score?

Soft inquiries, which include screening reviews, do not affect credit scores according to the CFPB; hard inquiries, which follow credit applications, can. Many tenant screening services use soft pulls, but pull types vary by provider, so confirm with yours before answering an applicant's question definitively.

This article is general information for Washington rental property owners, not legal advice. Screening laws change and vary by city; consult an attorney for guidance on your specific situation.

How Sagareus Handles Tenant Screening

Set the criteria up front, then apply them identically to every single applicant. Consistency is the whole game. The fastest way to a Fair Housing complaint, or a non-paying resident, is making an exception on a gut feeling. Here is how we keep it disciplined:

- Written criteria, fixed up front. Income, credit, rental history, and background standards are defined in advance, so no one is improvising once a name is attached.

- The same checks for everyone. Every applicant runs through the same review, in the order applications are completed, with verified income and documentation held to one standard.

- A second set of eyes before any decision. An assistant gathers and verifies; a leasing lead reviews the file for inconsistencies before it is approved or declined.

- Documented decisions, lawful notices. Every approval or decline is written down with its reasons, and anyone turned down receives a proper adverse-action notice.

We screen under the Fair Housing Act, Washington law, and local ordinances, including source-of-income and fair-chance rules. Lawful income like a housing voucher is counted, never penalized.

You get a real, repeatable system, not a hunch. That is what protects your home and your residents.

For the full screening framework behind these steps, see our pillar guide to tenant screening in Washington State.

Related Sagareus Services: